Ability to Pay

These questions might help determine your “ability to pay” based on Tillamook Habitat guidelines or Third party lender standards.

These questions might help determine your “ability to pay” based on Tillamook Habitat guidelines or Third party lender standards.

- Have you owned a home in the last three years?

Many first-time buyer programs, such as the matched savings program, require 3 years post-ownership in order to qualify for funding. This is not an issue however, if you answered yes

- Is your income steady?

A Steady Income means: no gaps in income stream for 2 or more years

- Are there gaps in your income stream for short periods once per year?

Short periods are defined as 3 months or less

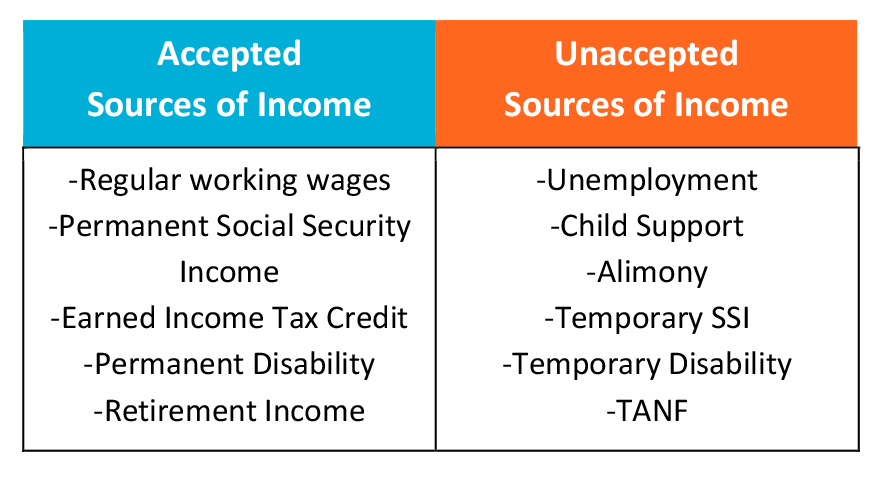

- Have you reviewed the sources of accepted/unaccepted income?

Habitat considers the following in calculating income:

- Have you paid rent on time for the past 12 months?

In most cases, paying your rent on time won’t help your credit score. In fact, the FICO score would ignore the rental trade line even if it appeared on your credit report. On the other hand, falling behind on your rent could lead to an eviction which would hurt your credit score and your ability to rent or get credit cards and loans in the future. There is an exception: some landlords may report payments to Experian Rent Bureau. In those instances, rent payments can help your Experian credit score.

- Is your utility payment history current?

Your credit score isn’t helped by timely payments on your utility or cell phone bills. However, if your account becomes past due, it may be passed on to a collection agency who would then list the account on your credit report leading to a credit score drop.

a - Do you have any accounts in collections?

If “YES” answer: We recommend that you begin credit counseling to establish goals for removing and/or paying off the accounts in collection.

- Do you have a deferred student loan?

If your loan is deferred, it is important that you have documentation regarding your deferred or income based payment plan, otherwise most lenders will assume 1-2% of the total loan amount as monthly payment.

- Are you able to save at least $1,000 towards closing costs?

We can assist you in signing up for a matched savings program. Your money will be matched three to one. In general, closing costs to purchase a home are estimated at around $4,000.

a - Do you know what your Debt-to Income (DTI) ratio is?

Your DTI ratio is your personal monthly budget and how much can be safely dedicated to home-related expenses. Monthly debt includes medical/dental, school loans (even deferred school loans), child support/alimony payments, car payments, loans, past due accounts. Does not include rent, utilities, or insurance.

See how to calculate it here